If you want to plan your own finances using Central Government schemes — or assist someone from a low-income or less-privileged background in managing and structuring their finances through government-backed programs — this post is for you.

When used strategically, these schemes can reduce financial risk, lower the cost of capital, strengthen savings discipline, and create long-term financial security.

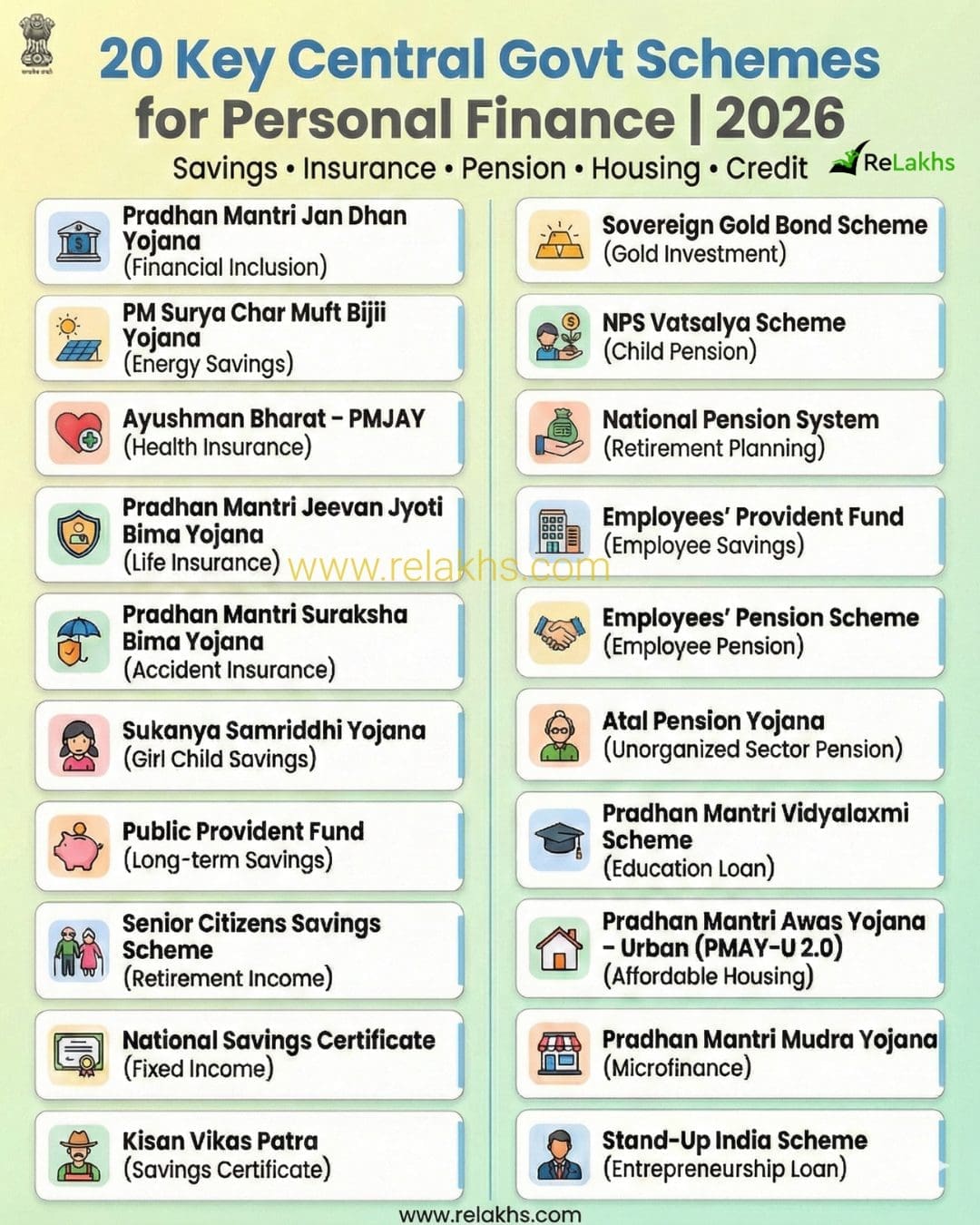

Below is a comprehensive list of Central Government of India schemes related to personal finance — covering financial inclusion, savings, pension, insurance, credit/loans, and investment-linked programs that individuals can use to manage, protect, grow, and plan their money effectively.

This guide consolidates 20 essential Central Government schemes and explains their key features, eligibility criteria, tax implications, lock-in periods, and withdrawal rules — all in one place.

20 Key Central Government Schemes for Personal Finance

Here are the five categories under which these 20 schemes can be divided:

- Foundation: Financial Inclusion & Structural Cashflow

- Protection Layer: Risk Management

- Stability Layer: Guaranteed Savings & Income

- Retirement & Long-Term Security

- Credit & Growth Optimization

Below is a structured breakdown of 20 key schemes, covering:

- Key Features

- Eligibility

- Minimum Investment / Premium

- Lock-in Period

- Tax Treatment

- Withdrawal Rules

FOUNDATION: Financial Inclusion & Structural Cashflow

1. Pradhan Mantri Jan Dhan Yojana (PMJDY)

Purpose: Universal banking access

- Eligibility: Any Indian citizen (10+ years with guardian)

- Minimum Balance: Zero balance

- Lock-in: None

- Features: RuPay card, overdraft up to ₹10,000, Direct Benefit Transfer access

- Tax: Savings account interest taxable (80TTA applicable)

- Withdrawal: Anytime

2. PM Surya Ghar Muft Bijli Yojana

Purpose: Reduce electricity expenses via rooftop solar

- Eligibility: Residential households

- Minimum Investment: Depends on system size

- Subsidy: Up to ₹78,000

- Lock-in: No formal lock-in, but asset-based

- Tax: Subsidy not taxable; electricity savings tax-free

- Withdrawal: Not applicable (capital asset)

3. Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PM-JAY)

Purpose: Health protection against major hospitalization expenses

- Eligibility: SECC-listed families (as per deprivation criteria) + all citizens aged 70+ years

- Coverage: ₹5 lakh per family per year (floater basis)

- Premium: Fully government-funded (no cost to beneficiary)

- Hospital Network: Cashless treatment at empanelled public and private hospitals across India

- Scope of Coverage:

- Secondary and tertiary hospitalization

- Pre- and post-hospitalization expenses (within defined limits)

- Day-care procedures included

- Lock-in: Annual coverage (renewed automatically for eligible beneficiaries)

- Tax: Not applicable

- Withdrawal: No cash payout — benefits available only through cashless hospitalization

- Best For: Low-income families, senior citizens without health insurance, households vulnerable to medical debt

PROTECTION LAYER: Risk Management

4. Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

- Eligibility: 18–50 years

- Premium: ₹436/year

- Coverage: ₹2 lakh

- Lock-in: Renewable yearly

- Tax: 80C deduction; payout tax-free

- Withdrawal: On death claim

5. Pradhan Mantri Suraksha Bima Yojana (PMSBY)

- Eligibility: 18–70 years

- Premium: ₹20/year

- Coverage: ₹2 lakh (accidental death/full disability)

- Lock-in: Annual renewal

- Tax: Premium eligible under 80C

- Withdrawal: Claim-based only

Note: Enrolment in the middle of the year (after June) now follows a pro-rata premium system (e.g., if you join in Dec-Feb, PMJJBY premium is only ₹228).

STABILITY LAYER: Guaranteed Savings & Income

6. Sukanya Samriddhi Yojana (SSY)

Purpose: Long-term savings for a girl child’s education and marriage.

- Eligibility: Available for a girl child below 10 years of age. The account must be opened by a parent or legal guardian. A maximum of two girl children per family are allowed (with exceptions in case of twins or triplets).

- Minimum Contribution: ₹250 per year, with a maximum contribution limit of ₹1.5 lakh per financial year. Contributions are required only for 15 years from the date of opening.

- Lock-in: The scheme matures when the girl turns 21 years old.

- Interest Rate: Approximately 8.2%, reset quarterly by the Government and compounded annually.

- Tax Treatment: EEE (Exempt-Exempt-Exempt). Contributions qualify for deduction under Section 80C within the overall ₹1.5 lakh limit. Interest earned and maturity amount are tax-free.

- Withdrawal Rules: Up to 50% of the balance can be withdrawn at age 18 for higher education. Full withdrawal is allowed upon maturity at 21.

- Best For: Parents looking for a disciplined, high-interest, tax-efficient savings option dedicated to their daughter’s future.

7. Public Provident Fund (PPF)

- Eligibility: Resident individuals

- Minimum: ₹500/year

- Lock-in: 15 years

- Interest: ~7.1%

- Tax: Exempt-Exempt-Exempt

- Withdrawal: Partial after 7 years

8. Senior Citizens Savings Scheme (SCSS)

- Eligibility: 60+ (or VRS 55+)

- Minimum: ₹1,000

- Lock-in: 5 years

- Interest: ~8.2% (quarterly payout)

- Tax: 80C eligible; interest taxable

- Withdrawal: Premature with penalty

Note: The maximum investment limit was increased to ₹30 Lakh per individual.

9. National Savings Certificate (NSC)

- Eligibility: Individuals

- Minimum: ₹1,000

- Lock-in: 5 years

- Interest: ~7.7%

- Tax: 80C eligible; interest taxable (deemed reinvested)

- Withdrawal: After maturity

10. Kisan Vikas Patra (KVP)

- Eligibility: Individuals

- Minimum: ₹1,000

- Lock-in: 2.5 years (but maturity doubles in ~115 months)

- Tax: No 80C benefit; interest taxable

- Withdrawal: After lock-in

Note: The current (Jan – Mar 2026) interest is 7.5%, doubling your money in exactly 115 months (~9 years 7 months).

11. Sovereign Gold Bond Scheme (SGB)

- Eligibility: Residents

- Minimum: 1 gram

- Lock-in: 8 years (exit after 5 years allowed)

- Interest: 2.5% annually

- Tax: Capital gains tax-free at maturity

- Withdrawal: Early exit window after 5 years

Budget 2026 update : Capital gains are only tax-free if you are the original subscriber and hold until the 8-year maturity. If bought from the secondary market, gains are taxable.

RETIREMENT & LONG-TERM SECURITY

12. NPS Vatsalya Scheme

Purpose: Early retirement planning and long-term wealth creation for minors through a regulated pension framework.

- Eligibility: Available for minors. The account is opened and operated by a parent or legal guardian until the child turns 18.

- Minimum Contribution: ₹1,000 per financial year, with no strict upper limit (subject to NPS guidelines).

- Lock-in: The account remains under guardian control until the child turns 18. Upon attaining majority, it seamlessly converts into a regular NPS Tier-1 account.

- Tax Treatment: Parent’s contribution qualifies for deduction under Section 80C within the overall ₹1.5 lakh limit.

- Withdrawal Rules: After conversion to a regular NPS account, standard NPS withdrawal rules apply — including partial withdrawals under permitted conditions and retirement withdrawal at age 60.

- Best For: Parents who want to start disciplined, long-term retirement planning early and leverage the power of compounding over decades.

Note : The account seamlessly converts to a standard NPS Tier-1 at age 18.

13. National Pension System (NPS)

- Eligibility: 18–70 years

- Minimum: ₹1,000/year

- Lock-in: Till 60

- Tax: 80C + 80CCD(1B) ₹50,000 extra

- Withdrawal: 60% lump sum tax-free at maturity

Note : You can also withdraw 25% of your own contribution for specific reasons (home, wedding, illness) after 3 years.

14. Employees’ Provident Fund (EPF)

- Eligibility: Salaried employees

- Contribution: 12% salary

- Lock-in: Till retirement

- Tax: EEE (subject to limits)

- Withdrawal: On retirement/resignation

15. Employees’ Pension Scheme (EPS)

Purpose: Provide lifelong monthly pension to salaried employees after retirement.

- Eligibility: Applicable to EPF members. A portion (8.33%) of the employer’s EPF contribution is diverted to EPS.

- Minimum Service Requirement: A minimum of 10 years of contributory service is required to qualify for monthly pension.

- Retirement Age:

- Regular pension payable from age 58

- Early pension allowed from age 50 (with reduced payout)

- Pension Type: Defined benefit scheme (pension amount is based on pensionable salary and years of service, not market returns).

- Withdrawal Rules:

- Monthly pension after age 58 (if 10+ years of service)

- If service is less than 10 years, withdrawal benefit available (no monthly pension)

- Nominee/family pension available in case of member’s death

- Best For: Salaried employees seeking guaranteed lifetime income post-retirement in addition to EPF corpus.

16. Atal Pension Yojana (APY)

- Eligibility: 18–40 years

- Lock-in: Till 60

- Pension: ₹1,000–₹5,000 guaranteed

- Tax: 80CCD eligible

Latest Update : The Union Cabinet has officially approved the continuation of the Atal Pension Yojana (APY) until the financial year 2030–31.

The interest rates mentioned for Small Savings Schemes (such as PPF, SSY, SCSS, NSC, KVP, etc.) are applicable for the January–March 2026 quarter and are subject to revision by the Government every quarter.

Tax deductions under Sections 80C, 80D, 80CCD(1B), and other provisions referenced in this article are applicable under the Old Tax Regime. These benefits may not be available or may differ under the New Tax Regime.

CREDIT & GROWTH OPTIMIZATION

17. Pradhan Mantri Vidyalaxmi Scheme

- Eligibility: Students admitted to eligible institutions

- Loan Limit: As per bank norms

- Subvention: 3% interest subsidy (eligible families)

- Tax: 80E on education loan interest

- Repayment: Post moratorium

18. Pradhan Mantri Awas Yojana Urban (PMAY-U 2.0)

- Eligibility: EWS/LIG/MIG

- Benefit: Up to ₹1.80 lakh interest subsidy

- Lock-in: Property occupancy conditions

- Tax: Normal home loan tax benefits apply

Note : The interest subsidy of 4% (up to a loan of ₹25 lakh) is available for EWS/LIG/MIG families for a period of 12 years, with a max benefit of ~₹1.80 lakh.

19. Pradhan Mantri Mudra Yojana

- Eligibility: Non-corporate small businesses

- Loan Limit: Up to ₹20 lakh (Tarun category)

- Collateral: Not required

- Repayment: As per bank terms

20. Stand-Up India Scheme

- Eligibility: SC/ST or Women entrepreneurs

- Loan: ₹10 lakh to ₹1 crore

- Purpose: Greenfield enterprise

- Collateral: CGTMSE coverage available

Government schemes are not random subsidies — they can form a structured financial ecosystem, if used well. The key is not to enroll in everything. The key is to use the right scheme for the right purpose at the right stage of life.

Before enrolling in any scheme, take a moment to carefully check your eligibility and verify the latest official interest rates, terms, and rules. Make sure you understand the lock‑in period and liquidity constraints, and assess whether the scheme truly aligns with your financial goals.

If you found this guide helpful, consider bookmarking it for future reference and sharing it with family members or friends who might benefit. You can also take this opportunity to review your current financial setup and identify any gaps or areas that need attention.

Continue reading:

- Do Small Savings Schemes Interest Rates Change Every Quarter? Fixed vs Variable Explained

- What’s in a Name? The Hidden Truth About Children’s Insurance Plans

- SBI ₹60 Lakh Personal Accident Policy for ₹3,000 Per Year- Worth it?

- LIC Policy Returns in 2026: How Much Do LIC Policies Really Return?

Disclaimer : This framework includes only currently active and structurally relevant Central Government schemes aligned to personal finance. Schemes that are purely sector-specific or targeted exclusively toward specific economic groups (for example, agriculture-only, industry-specific, or welfare-exclusive programs) have not been included. Some popular schemes (such as Mahila Samman Savings Certificate) and other discontinued or time-bound schemes have been intentionally excluded to maintain accuracy and long-term relevance. These schemes may be modified, expanded, restricted, or withdrawn if there is a change in government or policy direction. Readers are advised to verify the latest official notifications, circulars, and eligibility conditions before making financial decisions. This framework is educational in nature and not a substitute for personalized financial advice. For more details on these schemes, visit myscheme.gov.in

(Post first published on : 19-Feb-2026)

Join our channels