In the latest Union Budget an additional Income Tax deduction of Rs 1.5 lakh on affordable home loans has been announced. A new Section 80EEA will be introduced under the IT Act.

As per the proposal, income tax payers will get maximum tax benefit of Rs 3.5 lakh on home loans of up to Rs 45 lakh borrowed upto March 31, 2020 (subject to certain terms & conditions).

Wow! A tax benefit of Rs 3,50,000? That sounds really good and beneficial to home loan borrowers. Is n’t it?

But, given certain eligibility conditions to claim this Rs 1.5 lakh additional home loan tax deduction, will it be really beneficial to the first-time home loan borrowers? Is it possible to claim full tax deduction of Rs 3.5 lakh in a Financial Year/Assessment Year? What is the utility of these home loan tax benefits of Rs 3.5 lakh? Let’s discuss….

How beneficial is Rs 1.5 lakh additional Home Loan Tax Deduction? What is the utility of Rs 3.5 lakh home loan tax benefits?

Let’s understand if one can make full use of Rs 3,50,000 tax benefit on home loans or not, including the new Rs 1,50,000 additional tax benefit u/s 80EEA;

- Firstly, the additional tax deduction of Rs 1,50,000 is for first-time home borrowers only. In case, you have an existing residential property, you can not claim tax benefit u/s 80EEA.

- The residential projects should have been approved on or after the 1st day of September, 2019. So, only new housing projects or under-construction projects are eligible. Also, such project should be the only housing project on the plot of land.

- Do note that your property should have a stamp duty value of maximum Rs 45 lakh (Stamp Duty Value). Only such properties fall under ‘affordable housing’ category. Notice that its the Registration value and not the ‘agreement value’. In majority of the property deals, there will be white and black money proportion (though this is legally not allowed).

- In metro cities, a property which does not exceed 60 sq mtr (645 Sq ft) is only classified under affordable housing. So, you need to see if that kind of small house is suitable for your living or not.

- To claim interest amount of up to Rs 2 lakh as tax deduction under Section 24, the home loan should have been taken from any financial institution or even from your friend/relative. That’s not the case with Rs 1.5 lakh additional deduction u/s 80EEA. To claim tax benefit u/s 80EEA, the home loan should have been taken from a Financial institution only.

- Let’s assume that you are OK with all the above points and meet the required eligibility criteria, can you still claim full Rs 3.5 lakh tax deduction on your home loan?

- On a Rs 45 lakh property, you may get a loan of up to Rs 40 lakh max (80% to 90% property value as loan amount).

- Even if you take a new home loan in say September 2019 for Rs 40 lakh with a tenure of 20 years @ 9% rate of interest, you will be able to claim around Rs 2.09 lakh only in FY 2019-20 under section 24 and section 80EEA.

- For the next FY 2020-21 / AY 2021-22, you can however claim full Rs 3.5 lakh as tax deductions. In FY 2021-22, you can again claim less than Rs 3.5 lakh only (assuming same interest rate).

- But, note that here your loan amount is the maximum possible amount and the tenure is 20 years. In case, your loan amount is lower than this and/or tenure is less than 20 years, there is a high chance that you may not be able to utilize the full tax benefit of Rs 3,50,000 on your home loan.

- Longer the loan tenure, lower the EMI. Shorter the loan tenure, higher the EMI. Of course, going by the same logic, for shorter loan tenures, the interest amount paid is also less as against the longer tenure loans, where the interest amount increases. If you opt for longer tenure just to save some taxes, you may end up re-paying more interest amount than the actual tax benefit claimed by you. Do note that the actual tax benefit is also dependent on your individual income tax slab rate.

The main and sole benefit that I can currently think of is – to claim tax benefit under Section 24, you should have received possession of your house (interest paid before possession is eligible for deduction over the next 5 years in 5 equal installments). Section 80EEA do not impose any requirement of possession or completion of construction. Therefore, Section 80EEA provides you immediate tax relief even if you have purchased an under-construction property.

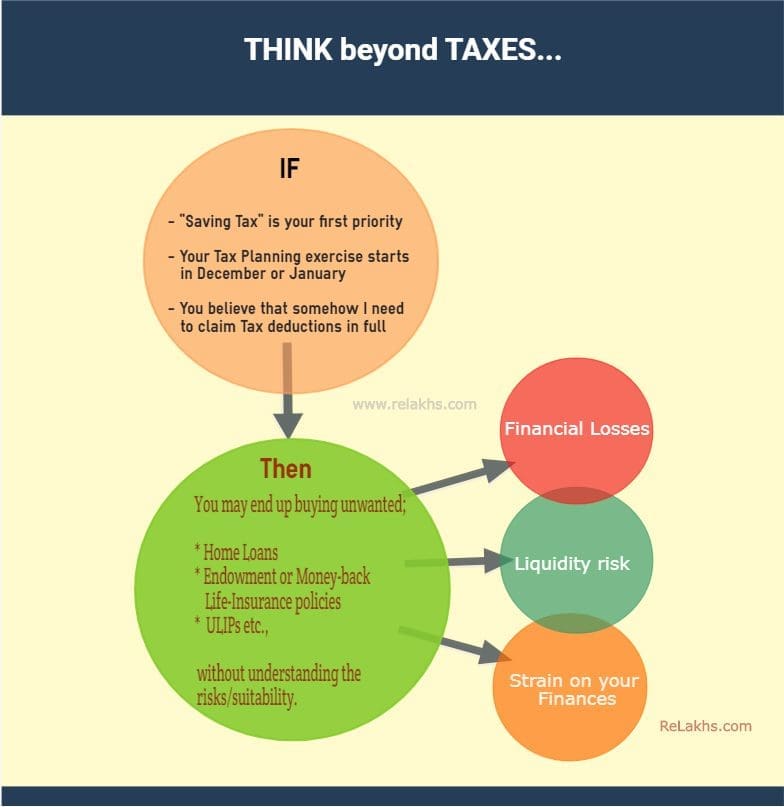

The main purpose of this post is neither to encourage or discourage to go for home loan. But, in the pretext of TAX SAVING, do not be in a hurry while taking important decisions. Tax planing is not Financial Planning! Think beyond TAXES!

A tax benefit of Rs 3.5 lakh on home loan interest repayments is surely making headlines! But, the actual utility of it can be very remote and majority of the first time home borrowers may note be able to make full use of it!

Continue reading :

- All in one guide to ‘Budget 2019-20 important Proposals’ related to Personal Finance | W.e.f AY 2020-21

- Income Tax Deductions List FY 2019-20 | List of important Income Tax Exemptions for AY 2020-21

- Income Tax Exemption Vs Tax Deduction Vs Tax Rebate Vs TDS | Key Differences

(Post first published on : 15-July-2019)

Join our channels

Thanks for such an amazing Article on how additional home loan tax deduction can be beneficial.

Thanks Sree. Exactly said about Tax planning is not Financial planning. One should plan beyond the Taxes.