As per the Finance Bill 2019, the threshold limit of tax rebate u/s 87A was revised to Rs 12,500 for FY 2019-20. This tax rebate has been made applicable if an individual’s (Resident Individuals including Senior Citizens) taxable income is less than or equal to Rs 5 Lakhs.

The Finance Bill 2020 (FY 2020-21) has kept this Sec 87A tax rebate unchanged for Assessment Year 2021-22 as well.

However, there is some confusion among the tax assessees as to whether Section 87A is available under both old & new tax regimes?

The Finance Bill 2020 introduced new tax regime, offers an optional lower rate of income tax to individuals with slab rates of 15% and 25% in addition to the 10%, 20% and 30% slab rates.

Individuals opting to pay tax under the new proposed lower personal income tax regime will have to forgo almost all tax breaks that you have been claiming in the old tax structure.

So, all deductions under chapter VIA (like section 80C, 80CCC, 80CCD, 80D, 80DD, 80DDB, 80E, 80EE, 80EEA, 80EEB, 80G, 80GG, 80GGA, 80GGC, 80IA, 80-IAB, 80-IAC, 80-IB, 80-IBA, etc) will not be claimable by those opting for the new tax regime.

But, what about the Income Tax Rebate of Rs 12,500 u/s 87A? Can you claim Sec 87A rebate under new tax regime for AY 2021-22?

Let’s now first understand what is the meaning of Tax Rebate?

What is Tax Rebate?

Tax rebate is a refund on taxes when the liability on tax is less than the tax paid or liable to pay, by the individual is referred to as Income Tax Rebate.

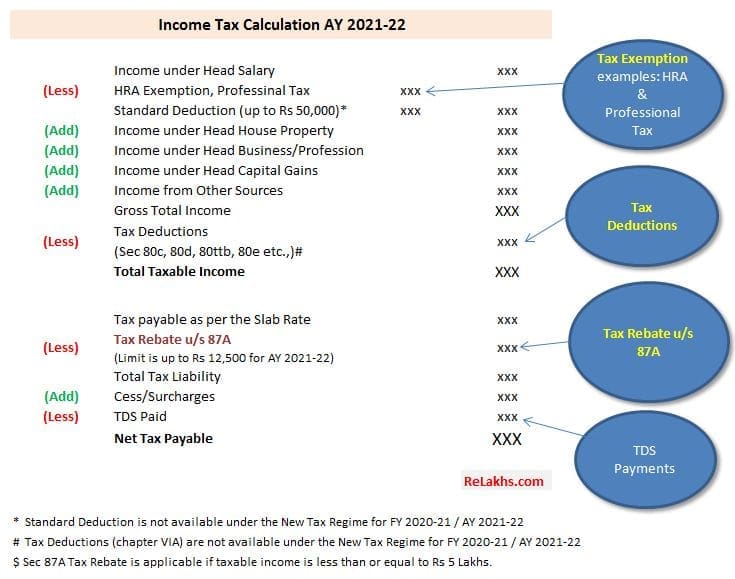

Income Tax Rebate Vs Tax Exemption Vs Tax Deduction

- Income Tax Exemptions are allowed to be claimed from a specific source of income (ex : Salary) and not from the Gross Total Income. Ex : HRA

- Income Tax Deductions are allowed to be claimed under each Head and also from Gross Total Income. The taxpayer can claim deductions in case he/she incurs specified expenditure or make specified investments under various sections of the IT Act. Examples: Investments u/s 80c (or) Health Insurance premium u/s 80D.

- Whereas, Income Tax Rebate is allowed to be claimed from the total tax payable. So, the exemptions and deductions are allowed to be claimed from the Income and Rebate is allowed from the tax payable.

Treatment & Applicability of Rebate under Section 87A AY 2021-22

Now that you understand what exactly is tax rebate, let’s jump to our ‘main topic’ as to whether you can claim Sec 87A Rebate of Rs 12,500 under both old and new tax regimes?

The answer is, YES. Section 87A Tax rebate is available under both new and old tax regimes for FY 2020-21 / AY 2021-22

Individuals having taxable income of up to Rs 5 lakh will be eligible for tax rebate under section 87A of up to Rs 12,500, thereby making zero tax payable in the Old and New Tax regimes.

Eligibility of Rebate U/S 87A Limit FY 2020-21

The threshold limit us/ 87A is Rs 12,500 for FY 2020-21 / AY 2021-22. This means that if the total tax payable is lower than Rs 12,500, then that amount will be the rebate under section 87A. This rebate is applied to the total tax before adding the Education Cess (4%).

- Only Individual Assesses earning net taxable income up to Rs 5 lakhs are eligible to enjoy tax rebate u/s 87A.

- For Example : Suppose your yearly pay comes to Rs 6,50,000 and you claim Rs 1,50,000 u/s 80C (available under old tax regime). The total net income in your case comes to Rs 5,00,000 which makes you eligible to claim tax rebate of Rs 12,500.

- The amount of tax rebate u/s 87A is restricted to maximum of Rs 12,500. In case the computed tax payable is less than Rs 12,500, say Rs 10,000 the tax rebate shall be limited to that lower amount i.e. Rs 10,000 only.

- The Tax Assessee is first required to add all incomes i.e. salary, house income, capital gains, business or profession income and income from other sources and then deduct the eligible tax deduction amounts u/s 80C to 80U and under section 24(b) (Home Loan Interest) to come up with the net taxable income. (If you opt for new tax regime then you can not claim income tax deductions u/s 80c, 80d etc.,)

- If the above net taxable income happens to be less than Rs 5 lakhs then the tax rebate of Rs 12,500 comes in to the picture and should be deducted from the calculated total income tax payable (as per the income tax slab rates applicable under old or new tax regimes).

| Taxable Income (Rs.) | Rebate u/s 87A |

| Rs. 3,00,000/- | 2500/- |

| Rs. 3,50,000/- | 5000/- |

| Rs. 4,00,000/- | 7500/- |

| Rs. 5,00,000/- | 12500/- |

| Rs. 5,00,100/- | Nil |

FAQs on Rebate under Section 87A AY 2021-22

- Can NRIs claim rebate under section 87A? – No, this tax rebate is only allowed for Resident Indians. Therefore, taxpayers qualifying as Non-Resident Indians are not eligible for a rebate under 87A.

- Can this rebate be claimed by a Firm or Company? – This rebate is only allowed to individuals. HUFs or firms or companies cannot claim this tax rebate.

- Are Cess & other charges (if any) need to be added before or after claiming this Tax Rebate? – Education Cess and SHEC are levied on the Tax payable after allowing for tax rebate of up to Rs 12,500.

- Is income tax rebate u/s 87A available on Long Term Capital Gains (LTCG)? – Rebate u/s 87A is not available on sale or transfer of equity shares i.e. on Long Term Capital Gains from equity or others as specified under section 112A. It is available on all other capital gains.

- Is rebate u/s 87A available on agricultural income? – Yes, income tax rebate u/s 87A is available on taxable income which includes agricultural incomes as well.

- My Taxable income is less than Rs 5 Lakh, so my tax liability would be NIL. Do I still need to file my Income Tax Return for FY 2020-21 / AY 2021-22? – You can avail of the zero tax benefit, but you still need to file your income tax return (ITR). The income tax exemption limit for all citizens below 60 years still remains at Rs 2.5 lakh. Therefore, if you are earning anything above these basic exemption limits annually then you are mandatorily required to file your ITR.

Continue reading:

- Income Tax Deductions List FY 2020-21 | New Vs Old Tax Regime AY 2021-22

- Health Insurance Sec 80D Tax Deduction FY 2020-21 / AY 2021-22 | Can I claim 80D Tax Benefit under the New Tax Regime?

- Latest TDS Rates FY 2020-21 | TDS Rate Table for AY 2021-22

- NPS Income Tax Benefits FY 2020-21 | Under Old & New Tax Regimes

(Post first published on : 02-January-2021)

Join our channels

It appears that no one including senior citizen with total income below Rs 5 lakhs has to pay tax after deductions under sec 47 A. Super senior citizens are not eligible for this claim. However are they still eligible for exemption of Rs 5 lakhs from tax. senior citizens and super senior citizens should be given tax eemption limits of Rs 6 lakhs and 7 lakhs respectively because sec 47 A gives exemption of Rs 5 lakhs to everybody less than 60 years old. Otehrwise sec 37 A is only a fraud.

S. Govindaswamy (89 years young)

Excellent feedback on Sce.87A. to the tax payers Sir.

Sir,

I am an Ex-Serviceman, I was discharged from service during Jun 2018. Since my case was premature discharge, my Pension Payment Order was finally received during Sep 2019. I had filed my tax return upto for the Assessment Year 2017-18. I have not filed the return for the AY 2018-19 and 2019-20. My basic pay for pension is Rs.29,400/- + DA. Now I am getting total Rs.34398/- every month. I have not yet started my second career. I have no other sources of income, except my pension. Now can I file the return for the AY 2020-21 and 2021-22 now.

Hi Sir,

I filled my income tax returns 2 months back. Still the Status is shown as Successfully e-Verified. Whether I need to Submit Grievance ?

Also in the For Your Action Tab, there is a action “Add/View Authorized Representative”. What is the action required for this ?

Dear Raj,

You may kindly for the ITR to get processed.

“Add/View Authorized Representative”, if you would have to file an ITR on behalf of someone else..

Related article : Income Tax Return of Deceased person | How to file ITR for the deceased as a Legal Heir?

very helpful…thanks for sharing…