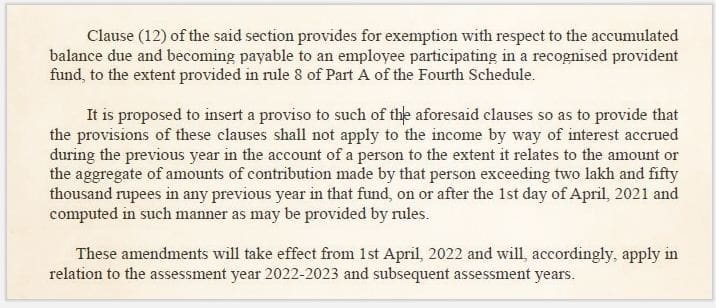

We are all aware that Budget 2021 (The Finance Bill 2021) has introduced one of the key amendments to the EPF Act. As per this amendment, from 1st April 2021 onwards, the interest on any contribution above Rs. 2.5 lakh by an employee to a recognized provident fund is taxable.

Until FY 2020-21, the interest income earned on contributions to EPF made by the employee was completely TAX-FREE.

Related Article : For more details, you may kindly go through this article @ Interest on EPF Contributions above Rs 2.5 lakh is Taxable | Budget 2021

In addition to the above amendment, the central govt has decided to implement the below important changes to the EPF act.

New EPF Rules 2021 | Latest Amendments

Below are the new EPF rules that EPF members need to be aware of;

- EPFO Aadhar Verification mandatory w.e.f. 1st June, 2021. (The last date to seed the Aadhaar number with UAN is extended from June 1, 2021, to September 1, 2021, for all EPFO beneficiaries.)

- EPFO hikes death insurance under EDLI scheme to Rs 7 lakh.

- EPFO allows its subscribers to avail the second COVID-19 advance (partial EPF withdrawal)

Let’s now go through these new EPF rules 2021 in detail….

EPFO Aadhar Verification mandatory w.e.f. 1st June, 2021

- The EPFO has instructed all the Employers (Company) that from June 1, if PF account is not linked to Aadhaar or UAN is not Aadhaar verified, then their ECRs (Electronic Challan cum Return) will not be filed. The last date to seed the Aadhaar number with UAN is extended from June 1, 2021, to September 1, 2021, for all EPFO beneficiaries

- This means, though employees can see their own PF account contribution, they will not be able to get the employer’s share.

- Also, if the accounts of PF account holders are not linked with Aadhaar, then they will not be able to use the services of EPFO.

So, hurry up, link your UAN to Aadhaar and get it verified.

EPFO hikes death insurance under EDLI scheme to Rs 7 lakh

In an another major amendment to the EPF act, the central govt has hiked the insurance claim amount under the EDLI scheme to Rs 7 lakh.

In a gazette notification, the Employees’ Provident Fund Organisation (EPFO) said the minimum death insurance has been increased to Rs 2.5 lakh and the maximum to Rs 7 lakh, from the earlier limits of Rs 2 lakh and Rs 6 lakh, respectively.

While the lower limit of Rs 2.5 lakh is coming with retrospective effect (w.e.f. 15th Feb, 2020), the upper limit has a prospective effect.

The Employees’ Deposit Linked Insurance Scheme (EDLI) is an insurance cover provided by the Employees’ Provident Fund Organization (EPFO). A nominee or legal heir of an active member of EPFO gets a lump sum payment of up to Rs 6 Lakhs (now Rs 7 lakh) in case of death of the member during the service period (active EPF member).

Related Article : How to make EPF Death Claim by Nominee of a Subscriber? | EPF/EPS/EDLI Scheme Benefits

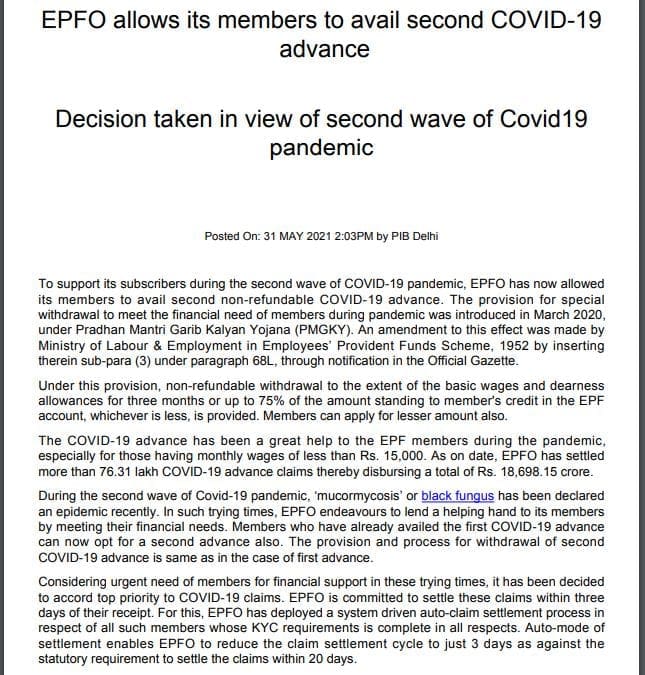

EPF advance (partial withdrawal claim) to combat Covid-19

EPFO allows all its members to avail second covid-19 advance (partial withdrawal).

Earlier last year (2020), the EPFO had allowed its members to withdraw COVID-19 advance to meet exigencies due to the pandemic. To support its subscribers during the second wave of COVID-19 pandemic, the EPFO has now allowed its members to avail second non-refundable COVID-19 advance.

The members are allowed to withdraw three months basic wages (basic pay + dearness allowance) or up to 75% of amount standing to their credit in their provident fund account, whichever is less.

The EPFO has settled more than 76.31 lakh COVID-19 advance claims thereby disbursing a total of Rs 18,698.15 crore as on date. If you have already availed the first COVID-19 advance, you can now opt for a second advance also.

Continue reading :

- Important & Comprehensive list of Budget 2021-22 Amendments related to Personal Finance | W.e.f AY 2022-23

- Provident Funds – Types & Tax Implications

- EPF Partial Withdrawals / Advances : Details, Rules & Guidelines

- Why should you Withdraw Old EPF Account Balance? | In-operative EPF A/c Timeline

- How to check if my Employer is depositing EPF amount with EPFO / Trust?

(Post first published on : 31-May-2021)

Join our channels

Is there any sealing of Rs.15000/month salary to be entitled for EPF?

Is there any sealing limit of Rs.6000/month irrespective of amount calculated w.r.t Basic+DA?

Sir what’s eligibility to withdraw EPS

Dear Chandan,

Below are the options for EPS withdrawals ;

If you have worked for less than 10 years and have been unemployed for more than 2 months then you can withdraw entire EPS balance (through Form 10c) along with EPF balance (Form 19).

If you have worked for more than 10 years then you can not withdraw full EPS balance. You can apply for Pension which starts either at 50 (early pension) or 58 years of your age.

In case, you resign from a job and join a new employer who does not offer EPF scheme then you can either withdraw EPS balance (if service history is less than 10 years) or apply for Scheme Certificate from EPFO.

You can submit this certificate when you join an EPF-covered organisation in future. If you do so, your service history gets carried forward.

If you don’t join an organisation and reach 50 or 58 years of age, you can submit these certificates (if employed with multiple employers) to the EPF field office under whose jurisdiction your last employer was covered and apply (Form 10D) for monthly pension.

In case, you resign from your current job and join a new organization where EPF scheme is offered, you can just submit Form-11 form to your new employer. Under this scenario, your EPF and EPS get transferred.

You may go through this article : What happens to EPS on Transfer of EPF account (or) when you switch Jobs?

Employee who joins as a fresh PF member on or after 1-Sep-2014 and the basic is above Rs.15000/- he or she cannot opt for EPS scheme. Is there any change in this scheme? If yes can share change please. If no the employee resigns from the present organization and joins another organization where the employee basic is less than Rs.15000/- or restricted PF of Rs.1800/- per month will the employee can become a Pension member?

Dear Chandrasekaran,

There is no change with respect to EPS elgibility criterion.

New EPF members enrolled on or after September 1, 2014, and having a salary of more than INR 15,000 month at the time of joining, will not become members of the EPS. Accordingly, the entire contribution of 24% (from the employee and employer) will go to the provident fund account of the employee.

I belive – if an employee at the time of joining the EPF scheme had a basic salary exceeding Rs 15,000 per month, then they cannot join the EPS at a later point too.

” So, if your salary is more than ₹15,000 per month, you will have to make an additional voluntary contribution to the EPS to get a higher pension”. 11th july 2023 was the deadline.

Dear Sir,

I have school running. What are criteria for PF registration like number of employees and their salaries. How much PF deduction from Employee salary and Employer Contribution and what are due date of deduction and submission of payment in PF Funds. Kindly guide me please …thanks

Dear Sanjay,

Request you to kindly engage a Chartered Accountant in this regard.

Organizations with 20 or more employees are required by law to register for the EPF scheme, while those with fewer than 20 employees can also register voluntarily.

Dear Srikant,

Can you please inform me that

1) What are the components on which EPF will be calculate?

2) Basic wages = Minimum Wages or not,

3) Rs 9804 is the current MW for west Bengal then what will be the minimum basic?

Samrat Chakraborty

incase a married male person died mother, father is also eligible for EDLI

Dear sankaramma,

You may kindly go through this detailed article – How to make EPF Death Claim by Nominee of a Subscriber? | EPF/EPS/EDLI Scheme Benefits

what is the contribution of epf if 12% from employee and 12% from employer if 12% contribution is Rs.1153?

in case a person leave the job for 12 months, can he claim the complete EPF? that is Employer and Employee contribution both?

Dear Kamal,

An EPF subscriber who is unemployed for 2 months or not contributing to EPF for more than 2 months, can withdraw full PF.

Read : Tax Implications of EPF, PPF & NPS Withdrawals (Full / Partial) & Maturity proceeds

Dear Srikanth ..I saw a comment from you that APY is not available to NRIs. I think that is wrong. The fact is , APY is not available to non citizens of India. NRIs still continue to be citizens till they surrender their citizenship which middle east NRIs do not do. Hence the question asked was can APY payments be deducted from an NRE account or NRO account , since NRIs are not permitted to open Resident SB account ?

Dear Safin,

Thank you so much for highlighting this point!

I stand corrected.

“Yes, NRI in the age group 18-40 years of age having a bank account with APY POP is eligible to open APY account.”

After opening of APY account, what will happen if a subscriber becomes non-citizen of the country?

The scheme is open to the Indian citizens only. Hence, in that event the APY account will be closed and the net actual interest earned on his contributions (after deducting the account maintenance charges) will be refunded, whereas, the Government co-contribution, and the interest earned on the Government co-contribution, shall not be returned to such subscribers.

Thanks Sreekanth.

Sreekanth, I am trying to reach you on Facebook message and gmail, Could you please check..