It’s that time of the year when you have to submit the Investment Proofs (Tax saving investments) to your employers. It is also the right time for most of the Life Insurance / Financial advisors to push financial products in the name of tax benefit and insurance cover.

LIC has launched its first new plan of 2021 called – LIC Bima Jyoti on 22nd Feb, 2021. LIC Bima Jyoti (Plan No.860) is a Traditional, Non-linked, Non-participating, Limited Premium Payment and Life Insurance Savings Plan.

Without any doubt, this plan may create quite a buzz in the market. The reason being its unique possible selling point (feature) – “pay premiums for limited period and get guaranteed additions (returns) on your Sum Insured.”

Given the low interest rate scenario, most of the retail investors would love to pick an investment option which gives them a better rate than Bank Fixed Deposits.

Under this plan, Guaranteed Additions shall accrue at the rate of Rs 50 per Rs 1,000 Basic Sum Assured at the end of each policy year throughout the policy term. That’s a 5% return! Wow!

Currently, an FD with one year tenure may not fetch you 5% return. So, Can LIC Bima Jyothi plan offer you better investment Returns? Is it the best LIC Savings Plan? What are the pros and cons of LIC’s new plan – Bima Jyoti Policy, let’s understand..

What is a Limited Premium Payment Insurance Plan?

A limited premium payment plan is a plan where you pay the premium for a shorter span of time and enjoy the benefits of an insurance cover for a long time.

The PPT under Bima Jyoti plan is Policy tenure minus 5 years. For example – if your policy term is 20 years then PPF will be 15 years.

What are Guaranteed additions?

The Guaranteed Additions are payable along with the Basic Sum Assured at the time of claim.

Under LIC Bima Jyoti plan, Guaranteed Additions are payable at the rate of Rs 50 per Rs 1,000 Basic Sum Assured at the end of each policy year throughout the policy term. This is part of your maturity benefit.

Related Article : Different types of Traditional Life Insurance Plans | Which one should you buy?

Eligibility Conditions under LIC Bhima Jyoti Policy

Below are the basic eligibility conditions of Bima Jyoti Plan;

| Minimum Sum Assured | Rs 1,00,000 |

| Maximum Sum Assured | No Upper Limit |

| Policy Tenure | 15 (or) 20 years |

| Premium Paying Term (PPT) | 10 (or) 15 years |

| Minimum Entry Age | 90 days |

| Maximum Entry Age | 60 years |

| Minimum age at maturity | 18 years |

| Maximum age at maturity | 75 years |

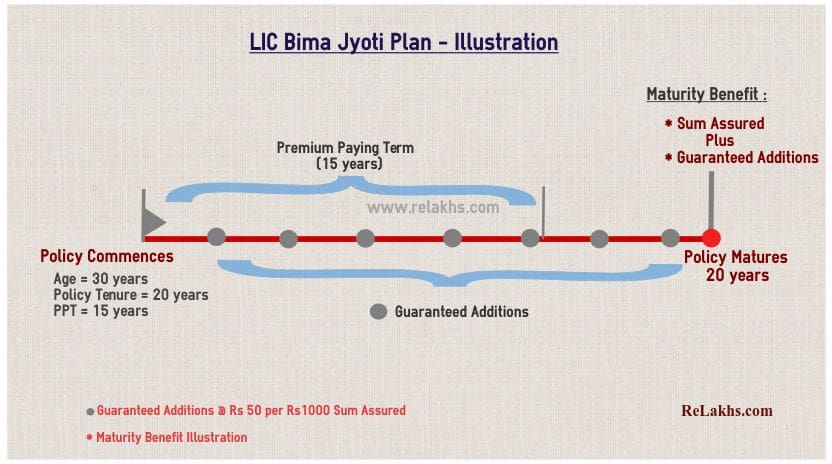

Illustration of LIC Bima Jyoti Plan

Assuming an individual takes Bima Jyoti policy with a tenure of 20 years for Rs 10 lakh sum assured. The premium paying term is 15 years.

A fixed GUARANTEED ADDITION at the rate of Rs 50 per thousand Basic Sum Assured gets accrued at the end of each policy year till 20th year.

At the end of policy tenure and on the life assured surviving to the end of the policy term, “Sum Assured on Maturity” along with accrued Guaranteed Additions, shall be payable as maturity benefit. (Where “Sum Assured on Maturity” is equal to the Basic Sum Assured.)

Maturity Benefit = Rs 10 lakh (Sum Assured) + Rs 10 lakh (Guaranteed Additions)

Guaranteed Additions Calculation = (Rs 50 x 20 x 1000000) / 1000

Kindly note that Bima Jyoti plan does not pay you any bonuses.

LIC Bima Jyoti Plan Returns Calculation

Let us consider an example – Mr Gupta (30 year) wants to invest in LIC’s new plan Bima Jyoti policy, with a Policy Term of 20 Yrs, Premium Paying Term 15 Yrs and for Sum Assured Rs 10 Lakh. The expected yearly premium will be Rs 82,545 (inclusive of rider premiums & taxes).

Let us now calculate Internal Rate of Return by considering the guaranteed additions that are payable for 20 years.

As per the above calculation, the expected returns from LIC Bima Jyoti plan would be around 4%.

Related Articles :

- Life Insurance Endowment Plan Return Calculation | Do-it-yourself guide!

- Life Insurance Money back Plan Return Calculation | Do-it-yourself guide!

LIC Bima Jyoti Plan – Should you Invest? | My Opinion

Kindly consider the below points before investing in LIC’s latest plan – Bima Jyoti plan;

- Guaranteed Additions are accrued : The Guaranteed additions offered under this policy do not have compounding effect. In the above illustration, LIC pays GAs of Rs 50 per 1000 of sum assured each year for 20 years. So, for a Rs 10 lakh SA policy, a total GA of Rs 10 lakh is payable at the maturity of policy. These guaranteed additions are just accrued till the maturity of the policy and compounding does not come into the picture. That is the reason why the returns are not 5% pa but they are around 4% only.

- Doubles your Sum Assured? : Your insurance advisor may highlight a point that your Sum Assured will double by the end of the policy tenure. In the above example, the SA is Rs 10 lakh and the GA is Rs 10 lakh. Please note that it’s just a sales pitch!

- Life Insurance Cover : The premium rates on Traditional plans are much higher than the term insurance plans. If you are buying an Endowment plan or money-back policy for life cover then kindly note that you are paying a very high premium for a low life cover. You can consider taking an online Term plan to get an adequate life insurance cover.

- Tax saving is an additional benefit : Insurance is primarily for Protection and not for saving Taxes. Kindly note that Tax saving is an additional benefit and should not be THE deciding factor when buying an insurance policy. Also, if you are opting for the new tax regime, note that you can not claim tax deductions u/s 80c.

- Erosion of wealth : Life insurance policies are long-term contracts. When you are investing for long-term, would you like to get decent inflation adjusted returns or not? Your endowment or money-back plans are low-yielding investments. These may give you negative inflation adjusted returns.

- Returns : If you are happy with 4 to 5% returns on your investment (with almost no risk factor & tax-free income), you can consider investing in these kind of plans. Else, you have plethora of investment avenues to consider.

I am sure you are now very clear on how much returns can we expect from these kind of traditional policies. The Investment Returns of around 4% that too over a period of 15 to 20 years sounds very low for me. Kindly be aware of the pros & cons financial products before you invest. Let me know your views. Do share your comments. Cheers!

Continue reading :

- LIC New Plans 2020 – 2021 List | Features, Snapshot & Review of all the Plans

- Top 5 Best Online Term Life Insurance Plans | Comparison & FAQs

- Income Tax Deductions List FY 2020-21 | New Vs Old Tax Regime AY 2021-22

(Post first published on : 19-February-2021)

Join our channels

Considering cumulative interest earned on the 15 nos. Rs. 82454/- premia paid and the maturity benefit as Rs. 20 L at 20 years, the effective ROI works out as 3.66%. It doesn’t seem wise to stick with such low interest for 20 yrs period. We never saw such low returns, so hopefully there may be higher return before 20 yrs period. If someone is looking for insurance cover, then it is better to go for simple term insurance for limited years.

LIC become a part of life to so many peoples . several tax saving schemes women plan children plan senior citizen plan etc … and this lic bima policy really a good one.

Yes. Earlier We could earn almost 170% of SA on 15 yrs endowment policy. The maturity amount included GA, LA and bonus. All tax free and with insurance cover.

Sir

Pls review

Bharti axa

Guaranted money plan

They are asking to pay the premium for 5 years nad from 7th year to 30 th year they will

Returns

Dear Amit,

May I know your requirements?

Are you looking for adequate life insurance cover and/or for better investment returns?

If returns, whats your expected rate of return?

Related article : Different types of Traditional Life Insurance Plans | Which one should you buy?

Your IRR calculation is incorrect. You are not paying money upfront but yearly. The IRR is more than 7%.

Dear Kushagra,

My calculation is based on the yearly payments only and not on ‘one-time’ payment.

The GA is Rs 50 per Rs 1000 SA ie 5%, how is it possible to get an IRR above 5%, could you kindly explain??

Actually LIC increased premiums from 84000 to 104000, I checked earlier and yesterday. So for 15 year policy term, the IRR went from 7.125 percent to 5 percent. Not an attractive policy now.

Dear Mr. Reddy,

Would we be correct in saying that following your exact calculations, but instead of 20 years, choosing a policy term of 15 years ( and hence premium payment term of 15-5=10 yrs ), gives us an attractive guaranteed return of 7.215% ?

Even more than PPF nowadays?

Dear Himanshu,

Kindly note that Rs 50 is GA which is 5%. As there is no compounding effect of GA, it is next to impossible to get returns beyond 4 to 5% from this plan, under all types of Plan options (15 year or 20 year).

Kindly recheck your calculations.

Dear Sir,

My friend has started investing in LIC Jeevan Umang for the past 2 years paying 4 lakhs per annum for a 15 year PPT. Not sure it is advisable to surrender the policy after the minimum 3 years mandatory premium payment. Do you advise him surrender this policy and plan for any alternate investment avenues (NPS/MF) . If so, Will the returns of the alternate investments, compensate the surrender charges/penalties/reduced returns, he will incur out of this policy surrender then? Please advice. Thanks.

Dear Ramesh,

May I know if he is the bread winner (earning member) of his family? Whether he has an adequate life insurance cover?

Related article: How much Term Life Insurance Cover do I need? | Online Insurance coverage Calculator

IT THE BEST PENSION PLAN LIC HAVE, i m an insurance advisor and i already taken this paying 2 lakh per year , i suggest don’t think about surrendering the policy, keeo it going as it is. its all for gud

In one point you mentioned that Insurance is primarily for Protection, so that means that focus should be on protection and not on returns. And in another point you mentioned that endowment or money-back plans are low-yielding investments.

You are negating your own point.

Aren’t you actually, confusing the reader?

Exactly bro..I also wish to bring the same point..

both the statement itself

is contradictory ..

Dear Hemant,

I have clearly mentioned the features of respective plans.

If your requirement is to get adequate life cover at affordable premium rate then Term plan should be considered.

If you already have sufficient cover and/or looking for a safe, tax-free long term savings plan and happy with 4 to 5% return then you can have a look at these kind of plans.

“Endowment or money-back plans are low-yielding investments” is a statement and not a suggestion.

LIC people Staff and authorities are enjoying in the customer’s money they does not bother of the customer LIC must be closed Totally useless except ITac rebate

this is ONLY TRUTH….everything is waste….ON PEOPLE MONEY EVERYONE ENJOYING ….

I don’t believe on this this is all the fake I take policy in 2001 and continue upto 2004 but unfortunately I did not continue it and to be 3 years one premiums was due my policy has been lapse this is ridiculous that the agent did not get the policy and my scheduled was busy I forget for this . Kya bata sakte hai ki agar aadmi Ke koi mishappening Ho jaaye aur vo apni policy na de paaye to uska paisa jo jama hai use milna chahiye na to aap policy k liye agent kyu bhejte ho mujhe mera paisa kyu nahi diya jaa raha hai iska kaaran bataye

Aap log logo ko loot rahe ho

I dont think somebody is looting someone…need of insurance is yours, protecting your beloved one from financial crisis in your absence is your responsibility not others..

plz dont blame others or transfer responsibility to someone else.

Dear Puran,

There is no ‘fake’ policy as such.

Either you have been ignorant about the features of the policy and/or your Insurance Agent might have mis-led you.

What r other products which gives guarantee , tax free returns with protection to the investment. Objective is long-term.

All are fake don’t take any policy from lic

Then which is real….tell me brother

Hello Puranji,

I think u don’t know about the details of ur policy. Ur pol document is simple an agreement with the Insurer and as u signed on the proposal form, it is very clear that u know the terms and conditions details. If the agreement is violated from ur side which is your mistake, for that u r not entitled to blame the company. Premium collection is not the exact duty of an LIC Agent. They all have no capacity to collect the cash as per rule.Only few unauthorised agents can collect cash amnt.U should have to collect all facts from ur agent which depend on ur trust % on him.Thnx a lot.

Dear Raju,

May I know the expectation of ‘return’ in this case?

My IRR working on through EXCEL gives IRR as 8%

Policy year Yearly premium Guarnteed Addition Net

1 -82545 50000 -32545

2 -82545 50000 -32545

3 -82545 50000 -32545

4 -82545 50000 -32545

5 -82545 50000 -32545

6 -82545 50000 -32545

7 -82545 50000 -32545

8 -82545 50000 -32545

9 -82545 50000 -32545

10 -82545 50000 -32545

11 -82545 50000 -32545

12 -82545 50000 -32545

13 -82545 50000 -32545

14 -82545 50000 -32545

15 -82545 50000 -32545

16 50000 50000

17 50000 50000

18 50000 50000

19 50000 50000

20 50000 50000

21 1000000 1000000

IRR 8%

Dear Alok,

Are you considering the Guaranteed Additions as ‘realized income’ for each policy year?

Sir log mehnat se paise kamate hai yeh log us paise ko kha jaate Hai

The are making fool

My be you becomes fool by your decision.