The Reserve Bank of India (RBI) has been cutting the key policy rates to mitigate Covid-19 impact. Also, most of the banks and financial institutions have already been reducing the interest rates on their deposits schemes.

So, as widely anticipated, the central Govt had previously announced a steep cut in the interest rates on small savings schemes for the first quarter (April to June) of FY 2020-21. Interest rates on various small savings schemes have been cut anywhere between 70 basis points and 140 basis points (100 basis points = 1 per cent).

However, the interest rates on small savings schemes have been kept unchanged by the government for the Second, third and fourth quarters of FY 2020-21.

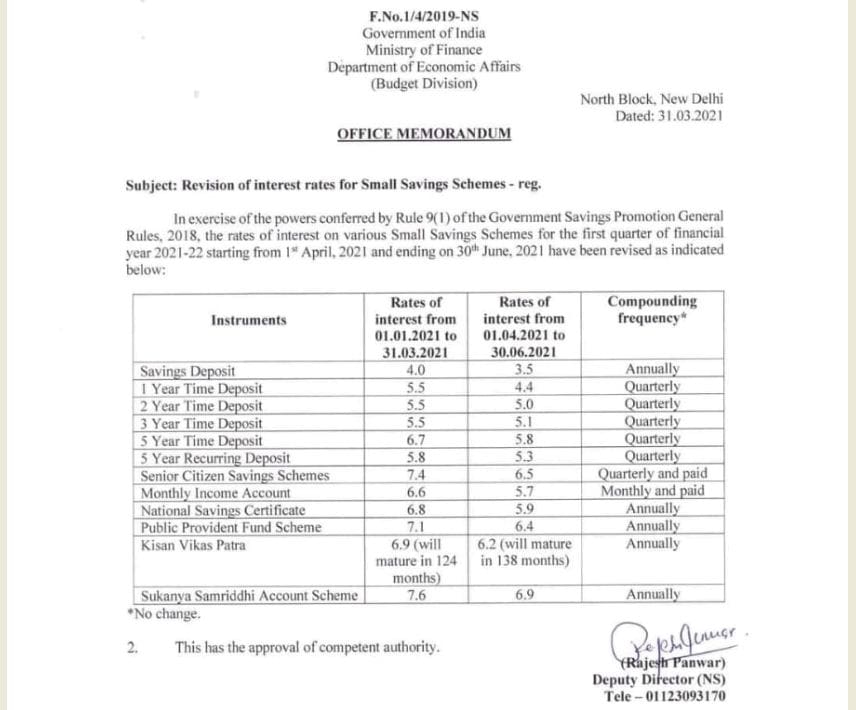

The Ministry of Finance on March 31 – 2021, announced a cut in interest rates for first quarter of FY 2021-22, in a host of schemes including small savings deposit rate, Senior Citizen Savings Scheme and Public Provident Fund Scheme.

These Small Saving Schemes interest rate cuts are in-line with overall interest rate movement in financial system. When bank lending deposit rates fall sharply, small savings rates have to follow to align with the larger trend.

(Latest News) | Govt withdraws Small Savings Scheme (SSS) rate cut.

Govt withdraws Small Savings Scheme (SSS) rate cut. The cut in interest rates have been rolled back!

Interest rates of SSS shall continue to be at the rates which existed in the last Quarter of FY 2020-21 (rates that prevailed as of March 2021).

The National Savings Schemes (NSSs) are one of the very popular saving schemes in India. These are regulated by the Ministry of Finance. They offer complete security of investment combined with attractive returns.

These schemes also act as instruments of financial inclusion especially in the geographically inaccessible areas due to their implementation primarily through the Post Offices, which have reach far and wide.

Some of the very popular schemes which fall under NSS are as below;

- PPF (Public Provident Fund)

- Sukanya Samriddhi Scheme

- Monthly Income Scheme (Monthly Income Account)

- Senior Citizen Savings Scheme

- KVP (Kisan Vikas Patra)

- NSC (National Savings Certificate)

- Time Deposits &

- Recurring Deposits

Latest Post Office Small Saving Schemes Interest rates Apr – Jun 2021 | Q1 of FY 2021-22

The latest rates of interest applicable (if rate cut has been implemented) on various small savings schemes for the quarter from April to June 2021 effective from 1.04.2021 would have been as below;

As the rate cut Order has been withdrawn, the latest rates are as below;

| Saving Scheme | Rates of Interest from 1st Jan 2021 to 31st Mar 2021 | New Rates of Interest from 1st April 2021 to 30th June 2021 |

| Sukanya Samriddhi Account -Girl Child Scheme | 7.6% | 7.6% |

| 5 Year Sr.CSS | 7.4% | 7.4% |

| PPF | 7.1% | 7.1% |

| Savings Deposit | 4.0% | 4.0% |

| 1 Year Term Deposit | 5.5% | 5.5% |

| 2 Year Term Deposit | 5.5% | 5.5% |

| 3 Year Term Deposit | 5.5% | 5.5% |

| 5 Year Term Deposit | 6.7% | 6.7% |

| 5 Year Recurring Deposit | 5.8% | 5.8% |

| 5 Year MIS | 6.6% | 6.6% |

| 5 Year NSC | 6.8% | 6.8% |

| Kisan Vikas Patra (KVP) | 6.9% | 6.9% |

Latest Interest Rate on Sukanya Samriddhi Scheme, PPF, MIS, NSC | Quarter-1 of FY 2021-22

The revised interest rates applicable on various small savings schemes for the first quarter from April to June 2021 effective from 1-04-2021 would be as below;

- The latest interest rate on Sukanya Samriddhi Scheme (SSA ) is 7.6%.

- The new rate of Interest on PPF (Public Provident Fund) would be 7.1%.

- The interest rate on Senior Citizen Savings Scheme (SCSS) has been reduced to 7.4%.

- New interest rate on Kisan Vikas Patra (KVP) would be 6.9%.

- The rate of interest on 5 year National Savings Certificate (NSC) is 6.8%.

- New interest rate on post office MIS (Monthly Income Scheme) is 6.6%.

- The rate of interest on a 5 year Post Office RD (Recurring Deposit) would be 5.8%.

Kindly note that interest rates of Small Savings Schemes are now reviewed and reset (if any) on a quarterly basis.

The revised rates (if any) are applicable for all the new investments MADE during the respective period.

For the existing investments under all the schemes (EXCEPT PPF & SUKANYA SAMRIDDHI SCHEME), the contracted interest rate remains unchanged until maturity.

Continue reading:

- 15 Q&As on Fixed Deposit Interest Income Taxation Rules

- LIC New Plans 2020 – 2021 List | Features, Snapshot & Review of all the Plans

- List of all Popular Investment Options in India – Features & Snapshot

- Top 15 Best Mutual Funds 2021 & beyond | Top Performing Equity Funds

- Income Tax Deductions List FY 2020-21 | New Vs Old Tax Regime AY 2021-22

(Post first published on : 31-March-2021)

Join our channels

Is fixed deposits in small pvt. banks are safe. Secondly where to invest to get monthly regular income already invested in sr.citizen scheam & PM VV Yojna & Post Office Monthly Income Scheam.Present age is 64 years. Advice Where to get maximum return on monthly basis , Having No Pension.

Really informative article. I am following your articles from couple of days & I must say that your articles are really knowledgeable.

Thanks for the update.

forex Beginner

Latest Small Saving Schemes Interest rates Apr – Jun 2021

best software provider for starting to open your own forex brokerage

Latest Small Saving Schemes Interest rates Apr – Jun 2021

NSC ARE BETTER OR BANK FIXED DEPOSITS. HOW MUCH SEALING OF AMOUNT ARE INSURED IN POST OFFICE AT PRESENT.

ig forex broker demo account

Latest Small Saving Schemes Interest rates Apr – Jun 2021

Forex explained

Latest Small Saving Schemes Interest rates Apr – Jun 2021

please sir give in money please

my account number:-5545064166

IFSC:-KKBK0000492

please gift money

my name RAHUL KHAN

my mobile number:-+919566980196

thanks for sharing

People of Hindoosthan have to understand that GOI is bankrupt,Banks are bankrupt.Therefore,the GOI HAS TO privatise and outsource – NOT TO RAISE CAPITAL – but to DOWNSIZE STAFF FOREVER.Those Jobs will go forever. dindooo hindoo

The Methodology is Simple – Take Banks,ports,Hotels … of GOI.`1st the GOI destroys these PSUs,by corruption and mismanagement and overstaffing – and then PAID NEWS IN THE BANIA MEDIA – HIGHLIGHTS THE “OPPORTUNITY” to PRIVATISE, and that the savings will be used for GAU MATA.Then comes in the “INDIAN CONSULTANT”, who is paid a bribe to make a PRIVATISATION RECOMMENDATION.

Then ANOTHER CONSULTANT IS HIRED,FOR RFQ/RFI/RFP,to rig the tender in favour of the pets of Chaiwala and Fat Pancho – Amit Shah.

Another SOP of Chaiwala ! Set up a sea port where there is NO SEA or an AIRPORT where a plane CANNOT LAND.So it will make losses. Losses are good,as it ENSURES THAT NO STAFF IS HIRED (which is a good excuse NOT TO HIRE).Then privatise – FOR THE REAL ESTATE.

FOR THE PSUs which are NOT privatised,the GOI INCREASES THE QUOTAS,BUT ALSO THE QUALIFICATIONS,AND THESE JOBS ARE NEVER FILLED (as the Dalits have no education and cannot pass or meet the standards). Total Job Destruction !

Then we come to the Banks,which are bust.What does the GOI do ? Demonetisation of deposits – through sleight of hand. 1st,REDUCE SAVINGS BANKS INTEREST RATES,so the BANKS GET RECAPITALISED BY PROFITS,and the POOR DEPOSITOR GETS NIL REAL INTEREST,AS THE “TINA” OPTION comes in.The Option is the DISASTER OF CHIT FUNDS AND CO-OPERATIVE !

By lowering bank savings interest,the govtt and corporate borrowing costs ALSO REDUCE.Corporate profits rise and the tax thereon,FLOWS TO THE GOI

SME and SME jobs ARE DESTROYED by GST and DEMO – as a part of a plan.EVEN COVID is AN OPPORTUNITY FOR THE STATE TO DESTROY SME.SME ARE A BURDEN ON POWER INFRA AND TAX INFRA.They pay No tax (GST and Profit Tax),No power,No PF,No ESI and deal in cash.All the SME business has gone to TYCOOONS,AND they are NOW PAYING TAX ON INCREMENTAL PROFITS.In the next BUDGET the TAX RATES ON THESE TYCOONS WILL BE LOWERED ! The Stock prices of these Tycoons has gone up and so has the STT earned by the GOI.SO THE DESTRUCTION OF THE SME HAS MET THE PURPOSE.

Agriculture is doomed.All inputs rate are up and farm gate prices are the same or lower.There is NO MSP in India.THE GOI HAS NO MONEY.THE GOI finds ingenious ways to,NOT PAY MSP.AI and Farm tebchology will DESTROY 90% OF INDIAN FARMERS.THEY ARE NOT REQUIRED ! ALL THAT THEY PRODUCE,CAN BE IMPORTED,AT HALF THE COST.THERE ARE NO JOBS FOR FARMERS – AS THEY HAVE NO EDUCATION OR SKILLS.THIS HUGE DISASTER WILL LOWER LABOUR COSTS (FOR THE BENEFIT OF TYCOONS)

Because of the LOOT of the BANIAS and MARWARIS over 70 years, EDIBLE OIL IS IMPORTED AT 100% DUTY,AND THERE IS A 200% TAX ON DIESEL ! And that is Y the savings banks rates,will go to NEAR ZERO – as the GOI needs the DUMB INDIANS,TO LEND MONEY AT ZERO RATES OR NEGATIVE REAL INTEREST RATES.

The RBI model is simple ! Con the DUMB INDIANS to put the money in banks (at close to zero rates),tax the interest,AND THEN LET THE BANIA COMPANY LOOT THE BANKS VIA LOANS AND PAY OFF THE NETAS.Y do the DUMB INDIANS put the money into banks ? Simple ! RBI has ensured that ALL OTHER OPTIONS ARE EITHER DISASTER (FRAUD) OR NO SECURED BENEFITS OR MUCH LOWER RATES.

The Last STEP of Chaiwala will be RETAIL.That will WIPE OUT THE BANIA SHOPKEEPERS AND BRING THE RETAIL PROFIT IN THE TAX NET !The excuse will be,that IT WILL RAISE FARM GATE PRICES !

NET CONCLUSION – THERE WILL BE NO GOVTT JOBS AND THERE WILL NO PRIVATE JOBS FOR THE SEMI SKILLED AND LOWER SKILLED PERSONS.

I do not blame Chaiwala – He has NO CHOICE ! And nor does Rakesh Tikait – except that Tikait does NOT REALISE that MSP is NOT the solution ! AGRI IS DOOMED – BY AI AND TECHNOLOGY – SOLUTION IS PARTITION !

If farmers get higher rates and higher yield,the GOI takes it back in the form of fertiliser and other prices (which lowers the subsidy bill).OUT OF ALL THE MONEY SAVED BY THE CHAIWALA – by KILLING THE JOBS,the farmers are paid a monthly dole of Rs 1000,AND THE FARMERS ARE MIGHTY THRILLED.dindooohindoo

Hi Mr Reddy,

Your website is quite informative.

I have a query: If I have two 5-year TDs (Rs 5 lakh & Rs 2 lakh) in Post Office and the annual interest earned is about Rs 48,200 (Rs 34,500 + Rs 13,700), and if my total annual income does not exceed Rs 2.5 lakh, do I have to submit Form 15G?

My local post office says 15G is not required for 5-year TDs.

Please advise.