It’s heartening to see an ever-increasing number of people take active interest in managing their finances. Supporting these people with information, tools, guidance and moral support are multiple bloggers, websites, Facebook groups, WhatsApp groups, etc. All of these are good signs, not just for the common investor, but also the industry as a whole.

As investors become better-informed, they’ll become more willing to step out of their comfort zone and invest in smarter, more complex investing options that suit their requirements. This, in-turn, could lead to better products and improved services from the industry.

But there’s one area, where I feel, more needs to be done. This is based on my readings and experiences on various forums that carry out “financial literacy” efforts. That area is “numeracy” related to financial investments. I feel, while all efforts are being done on financial literacy are encouraging, we should not neglect the crucial aspect of numeracy, which influences almost every financial decision that we take.

Most people who are learning to manage their finances will be familiar with investment facts and figures. For example, they may know that investing in the right share or mutual fund can give a better return than an FD, although the risk will be higher. Similarly, they could assert that insurance as an investment option gives paltry returns. But the moment this same information is presented in numerical terms, their knowledge can be severely tested and they could even take the wrong decision.

Importance of numeracy in becoming Financially Literate

Let’s look at a few examples to understand this.

Case 1: Everyone knows that investing in the right shares can give you better returns than FDs. But let’s look at it from a numerical point of view and see if we reach the same decision? The first investment is in a share that has grown from Rs. 50 to Rs. 75 over a period of 3 years. The other investment is an FD that has given you a return of 9% over a period of 3 years. Can you compare the two investments and say which has actually given a better return?

Case 2: You plan to create a fund of Rs. 5 lakh in the next 4 years. After meeting your personal expenses, you know that you can save and invest Rs. 10,000 per month. There are two investment options available to you. The first scheme offers you 8% interest compounded annually and the return is almost guaranteed. The second option offers 11% compounded interest but there’s a higher risk associated with it. How many years will each of these investment options take to achieve the target amount? Will the safer option work or will you have to take the riskier option?

Case 3: You are being offered an attractive investment option by an agent where you have to pay just Rs. 8,000 per month for 20 years, at the end of which you’ll receive Rs. 30 lakhs. Is this a better option than investing in an RD? Consider tax treatment for both being the same.

Case 4: You have to compare the performance of 2 shares. One has grown by Rs. 11 (from Rs. 55 to Rs. 66) while the second one has grown by Rs. 220 (from Rs. 2780 to Rs. 3000). Which one has performed better?

Case 5: You have to create a corpus of Rs. 20 lakhs by the end of 5 years. You are only considering safe investment options and are therefore targeting a return of 8% per year. What is the amount you’ll need to invest to achieve your target keeping these factors in mind?

These are typical financial situations that you’ll face on your investing journey. Most of you may have even faced such situations. If you are truly literate, you should be able to arrive at the correct answers to all these questions. If you are not able to figure out how, then, you can only consider yourself half-good at the job. To take really informed financial decisions, you should be able to find what the numbers reveal.

Tackling numbers is, however, what turns off most people. Many people have grown up with a dread for numbers – a failure of our education system, more than anything else. The good news is that becoming comfortable with numbers doesn’t require a major reboot. You just need to know a bit of Excel and you’ll be on your way to start tackling such questions.

As someone who was always scared of numbers and was never comfortable with Excel, I can assure you that if I could learn to do it, anyone can do it.

So let’s look at each case and solve them one by one.

Case 1

There are different ways to solve this. We’ll take the easiest way.

Option a)

Let’s assume we bought Rs. 1 lakh worth of shares at Rs. 50 each. This would have given us 2000 shares. At the end of two years, the value of these 2000 shares will be Rs. 1,50,000 (75 x 2000).

Initial investment = Rs. 1,00,000

Present value = Rs. 1,50,000

Option b)

Let’s see how much we earn from our Fixed Deposit. To do this, we can use the Future Value (FV) function of Excel.

To do this, we will first have to enter the details that we know. These include

- Principal amount = Rs. 1,00,000

- Period in years = 3

- Interest rate = 9%

Then enter the Excel formula for calculating Future Value (=FV()) in the following cell. The moment you type the formula, Excel will show the following details;

= FV(rate,nper,pmt,pv,type)

Instead of entering the values directly, you can enter the cell references for each value.

So you have

Rate = C4

Nper = C3,

Pmt = 0 (this is if you are investing on a per month basis),

PV = C2, and

Type = 0 (you can ignore for the moment)

Then just press Enter.

You’ll get, Future Value = 1,29,502.90

Now, we know numerically that the investment in the stock was clearly better.

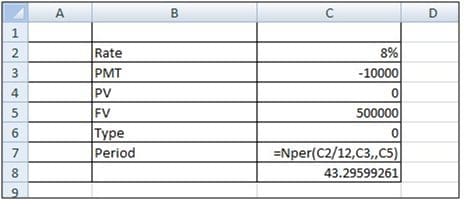

Case 2

You have to create a corpus of Rs. 5 lakh in four years. How much time will it take if you invest Rs. 10,000 per month at the rate of 8% and 11% compounded interest, respectively? Enter the details in the respective cells and then enter the formula for period (Nper) which is =Nper(rate,pmt,pv,fv,type)

Enter the details in the respective cells and then enter the formula for period (Nper) which is =Nper(rate,pmt,pv,fv,type)

Where,

Rate = C2/12 (we divide this by 12 as we are making monthly investments)

Pmt (investment per month) = C3

Target amount (future value) = C5

You can leave PV (present value) and Type as 0 or ignore them.

Then press Enter.

The answer you get is 43.29 months. That’s less than 4 years (48 months).

Since we can achieve the target of accumulating Rs. 5 lakh using the safer investment option, we needn’t calculate the period it will take if we invested at 11% interest. If we still want to know, we can use the same formula and just change the interest rate in cell C2.

Case 3

This is something we come across very frequently – usually from those selling insurance-cum-investment options. Let’s see how it works.

You have the following information;

Amount invested per month = Rs. 8,000

Tenure = 20 years

Future value = Rs. 30 lakh

Using the Rate function in Excel, we can easily calculate the rate of return. The formula for rate is =rate(nper,pmt,pv,fv,type,guess)

The formula for rate is =rate(nper,pmt,pv,fv,type,guess)

Entering the details as shown above, you’ll get the answer as 0.35%.

We’ll have to multiply this by 12 as we are making monthly payments.

Once we do this, we get the answer as 4.20%.

This is much lower than the returns you’ll earn from any RD.

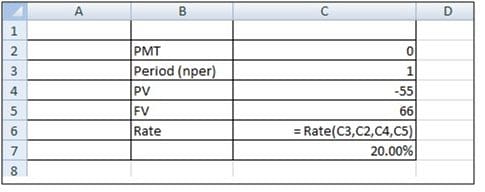

Case 4

Many people look at absolute numbers when comparing figures. This happens especially with share prices and mutual fund NAVs. People always want to invest in “lower priced”shares or mutual funds as they feel these investment options have the potential to “grow more” and thus give better returns. It’s something people should learn to look past. This example illustrates that misconception. (Read related article : ‘Should you avoid Mutual Funds with higher NAVs?‘)

Option a)

Initial Value (PV) = Rs. 55

Present Value (FV) = Rs. 66

Period = 1 (assuming the growth happened in one year)

Using the Excel rate formula, we can easily calculate the rate.

Growth in percentage terms = 20%

Option b)

As shown in the earlier example, we can replace the values and find the rate of growth for the second stock.

Initial value (PV) = Rs. 2,780

Final value (FV) = Rs. 3,000

Growth in percentage terms = 7.91%

(Make sure you always enter the initial value as negative number as otherwise Excel will give an error.)

This makes it clear that although numerically the growth is lesser, in terms of percentage, the first stock has given you vastly superior returns.

So, if you had invested Rs. 1 lakh in both investment options, the amount you’ll have currently is Rs. 1,20,000 and Rs. 1,07,910 respectively.

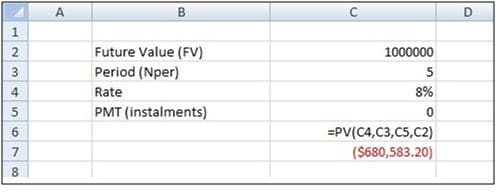

Case 5

This is a scenario we are very likely to face while investing. We all plan to invest for some specific goal and we need to understand how much we need to invest initially. Let’s look at how we can find this amount.

Future value = Rs. 10 lakh

Period = 5 years

Growth rate = 8%

The amount you should invest right now is Rs. 6,80,583.

If you were able to solve all the above questions, I congratulate you. There are many more formulas that you can explore to resolve many of the financial challenges you’ll face. For those who struggled a bit, please look at it as a gentle nudge to understand essential formulas that will help you take better investment decisions. Most of these formulas are in-built in MS Excel. You can check how they work on YouTube or take a course that teaches you Excel. It will be well worth the effort. I wish you the very best on your financial journey!

This is a Guest Post by Vinod of investjunction.co.in .

About the Author

Vinod Pottayil is the author of the book ‘What Every Indian Should Know Before Investing’. The book is currently in its fourth edition and available in leading book stores and online stores.

He also writes on his blog www.investjunction.co.in.

Continue reading :

- What is Time Value of Money?

- Personal Financial Calculators – Tools to manage your Finances more easily!

- 5 important Formulas to calculate Return on Investments

- How to calculate RoI using XIRR Function?

Kindly note that ReLakhs.com is not associated with investjunction.co.in. This is a guest post and NOT a sponsored one. We have not received any monetary benefit for publishing this article. The content of this post is intended for general information / educational purposes only.

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post published on : 20-November-2017)

Join our channels

Thank you for the article. It was really very helpful. All my doubts regarding numerical literacy are cleared now.

Dear sir,

My PPF account is going to be matured in this April.

I am in a dilemma to continue it for 5 more years or take 50% money and invest it in liquid fund. What do u suggest on that?

FYI i am 40 years old and right now money is not required to purchase anything?

Thanks

Manoj

Dear Manoj,

Then you may consider extending the time-period of the PPF ac.

Thnk you sir

Hi there,

Humbel request to you guys, I’m using screen reader which reads out for visually impaired. it doesn’t read graphic and images, hence pls make info in text. Above article is informative yet couldn’t relish full as excel examples are in graphic format(in between) explaination.

Thanks guys.

Dear Sir,

Amount invested per month = Rs. 4,000

Policy Term = 25 years

Premium payment term = 16 Years

Future value = Rs. 30 lakh

how to calculate rate of return above case. Because monthly payment is Rs. 4000 Pm X 16 Years but received amount at 25 Years.

Thanks

Dear Sridharan,

You can use IRR formula in Excel to calculate this.. (Internal Rate of Return).

You may visit my reviews on Insurance products to understand this calculation.

Sridharan,

Sreekanth is right. If you have regular payouts, you can use the IRR formula to calculate the returns. Although since your payments are monthly in nature, you’ll have to convert them into Annualized Returns by modifying the formula a bit. The formula will be = [1+IRR(Investment Value Cell Range))^12-1. This will give you the annualized rate.

Or you can simply use the XIRR formula and get the annualized rate of return by selecting the Investment values and Periods of Investment. You won’t have to convert it to annualized.

Hope this helps.

Thanks for both reply… i am understood..

I really loved this reading. I’m currently abroad and tried investments for almost 2 years and got lot of knowledge and also money return. But there is really so much to learn. I really like to thank you for this well articulated article with examples. Please keep up your good work.

You should really try approaching some college lecturers to translate your book contents to different languages so that it will reach all around India and it’s much needed. and try making audio series(podcasts) these will be good, People can hear using mobiles on their leisure time.

PG,

Thanks for sharing your thoughts. I’ll definitely see if I can work on some of these ideas.

Have a great day!

Dear Sir,

Nice article.. I have one doubt sir regarding in Mutual fund – CAGR any formula in excel …

Thanks…

Sridharan,

Thank you for your comment.

Regarding your question, you can calculate CAGR of Mutual Funds by using the XIRR formula in Excel. Here’s an article that I found on this site that explains how it works: https://www.relakhs.com/xirr-calculate-investment-returns/

You could use the Rate function too if you want to calculate a one-time investment. But the XIRR formula is more versatile as it works fine for both one-time investments as well as periodic investments that you are more likely to do with Mutual Funds.

There are tons of videos on YouTube and other Excel sites that will teach you how to use this formula. You simply need to enter the dates and your investments (negative number) and withdrawals or value of the investment (positive numbers) to get the compounded annual growth percentage.

Hope this helps.

Dear Vinod sir,

Thank you for your valuable reply….

Dear Sreekanth,

Very well explained and easy to understand. Vinod Pottayil has made financial understanding so easy. One small doubt i have;

CASE 4:

Assuming both shares are of Standard companies with healthy financial conditions, Don’t u feel that we should buy shares with less face value company? i feel it wont take much time from becoming 55 to 110, say may be 3 years, but share from 2700 face value to become 5400 takes much more time in Indian stock market scenario. What i mean is share with less face value doubles faster than higher face value, by simple mathematical calculation. Do U agree?

regards

RAJ

Raj,

Thank you for your comment.

Regarding your question, I will have to disagree with your assumption. Mathematically speaking, both would double – so it’s the same.

Realistically speaking, we just cannot compare two different stocks based on their prices and assume that the lower priced share will double quicker than the higher priced stock. This misconception is one reason why people sometimes get misled into buying very low priced stocks (below Rs. 10, for example) as they feel even a few rupee jump can make a huge difference. Assume you buy Rs. 1 lakh worth of a share priced at Rs. 2. Now, if the price jumps to Rs. 4, your investment doubles to Rs. 2 lakh! The journey from Rs. 2 to Rs. 4 seems so small in terms of numbers. But in terms of percentage, it’s as huge a jump as Rs. 500 to Rs. 1,000.

If you look into the past, higher priced stocks like Infosys, HDFC, JSW Steel, etc. have been growing at a fast clip. If you look at many of the well-performing medium-priced stocks, you’ll see that many have undergone stock-splits so that they appear more affordable to buy. For example, Infosys is around Rs. 900 and JSW Steel is around Rs. 260. Which is more expensive? If you look at their face value, Infosys has a face value of Rs. 5 while JSW Steel is Rs. 1. If Infosys goes for 1:5 split, its price would be around Rs. 180. Suddenly, Infosys will appear cheaper than JSW Steel. JSW Steel itself was around Rs. 1800 before it underwent a 1:10 split, recently. So just looking at the stock price without looking at face value can also confuse investors.

That said, lower stock price does increase trading frequency as more people may find it affordable to buy. This can have an impact on the stock price. But it cannot be a major impact as per my understanding. If you are looking at similar companies in the same industry, the smaller player maybe more nimble and therefore perform better. This could lead to quicker growth and therefore better performance on the stock market. But this growth will be mostly tied to its performance and a small part will be due to the lower price. I do not see any other inherent advantage in being lower priced.

Personally, for me, the price of a stock will not be a key factor. The company’s performance and other factors influencing the company, the industry it belongs to, market sentiments, etc. will be more important factors for me. I hope this helps in answering your question in some way!

Wow! can’t get a better insight than this!

Thank you dear Vinod for a detailed reply.

Thank you both for this nice explanation and reply

regards

RAJ

Thanks shrikanth for refresh this things very useful information shared.

It is not numerical literacy which is the main hindrance in achieving financial freedom. The main deterrent to financial freedom is the ability to comprehend a foreign language.

‘Relakhs’ always provide excellent articles on financial awareness and education. Unfortunately, all of this information reaches to a limited audience, who are fluent in English.

Incredibly smart and talented people of India miss out, because they find it hard to grasp English. The same article, if available in their mother tongue would make a lot more sense to the masses.

For example, my uncle who recently retired was looking for financial advice. So I sent him the articles on “Relakhs”; unfortunately he found it difficult to comprehend the article, because it was in English.

Kunal,

Great observation. I cannot agree with you more on this. In fact, there is hardly any publication devoted to investing and personal finance in regional languages. I realize that this is a huge gap and I’m surprised that not many organizations – private or government – are addressing it. I wanted to translate my book into multiple languages for the same reason but found it difficult for many reasons.

That said, numeracy issues remain, irrespective of which language you are comfortable with. Maths is a language unto itself and if you are not comfortable with it, you do hit a dead end while investing.

Thanks Vinod sir for your reply.

I do agree that numerical literacy plays a significant while taking financial decisions.

The reason behind my observation was only because I felt strongly about the shortage of information in regional languages. Hopefully my view did not came across as offensive, I did not meant it that way. My sincere apologies, if that has been the case.

In fact, I read nearly all articles on “Relakhs” as they are thoroughly researched, well articulated and written by very knowledgeable authors and I would like to thank them for the same.

Kunal,

Please be frank with your views. There was nothing offensive about your comment. And I agree that this site has amazing content for all investors!

Do keep reading and sharing your views!

Dear Kunal,

I too endorse your views.

We infact tried to provide a ‘translation tool’ (courtesy : Google) on our blog, but due to some technical challenges had to remove it for the time-being. We have also noticed that the translation is not up-to-the-mark, which may lead to even more confusion.. but will surely check with my tech team on how to go about this..

I have always believed that ‘willingness & determination’ matter a lot, if we have the willingness to learn, language should not be a major barrier. Even the well-educated individuals who are good at English, do give less importance to numeracy. There are ‘n’ number of people who believe that ‘one should not invest in higher priced stocks’….its just a misconception!

By the by, how about you spending sometime with your Uncle to make him understand the concepts that he would like to know/learn… I am sure, you can do your bit in spreading the knowledge with our friends/well-wishers.

Thanks for sharing wonderful views! Keep visiting!

We need to thank Vinod ji for sharing this wonderful article.