The cost of inflation index (CII) for the financial year 2021-22 has been notified by the Ministry of Finance. The ministry has set the Cost Inflation Index FY 202-22 as 317. For the previous FY 2020-21, CII value was 301.

The rate of inflation for indexation purposes is specified by the Indian Government for every financial year.

The base year is considered as 2001-02.

The base year was shifted from 1981 to 2001 in Budget 2017.

This CII number is important as it is used to arrive at the inflation adjusted purchasing price of assets (indexed cost of acquisition) which have been sold or planned to be sold in FY 2021-22.

The indexed cost of acquisition is used in the calculation of Long-term capital gains (LTCG) or Long Term Capital Losses (LTCL).

Kindly note that CII is used to calculate inflation-adjusted cost only for those assets where inflation-adjusted (indexation benefit) is allowed. For example, in the cases of debt mutual funds, real-estate property, gold etc.,

The CII value cannot be used to arrive at LTCG/LTCL on equity mutual funds. Index benefit is not allowed in case of bonds or debentures except capital indexation bonds or sovereign gold bonds issued by the RBI.

Latest Cost Inflation Index FY 2021-22 | CII Chart AY 2022-23

Below is the table of Cost Inflation Index numbers, as stipulated by the Income Tax Department. You can take values from the table to compute the indexed or inflation-adjusted cost of acquisition.

| Financial Year | Assessment Year | Cost of Inflation Index (CII) |

|---|---|---|

| 2001-02 (Base year) | 2002-03 | 100 |

| 2002-03 | 2003-04 | 105 |

| 2003-04 | 2004-05 | 109 |

| 2004-05 | 2005-06 | 113 |

| 2005-06 | 2006-07 | 117 |

| 2006-07 | 2007-08 | 122 |

| 2007-08 | 2008-09 | 129 |

| 2008-09 | 2009-10 | 137 |

| 2009-10 | 2010-11 | 148 |

| 2010-11 | 2011-12 | 167 |

| 2011-12 | 2012-13 | 184 |

| 2012-13 | 2013-14 | 200 |

| 2013-14 | 2014-15 | 220 |

| 2014-15 | 2015-16 | 240 |

| 2015-16 | 2016-17 | 254 |

| 2016-17 | 2017-18 | 264 |

| 2017-18 | 2018-19 | 272 |

| 2018-19 | 2019-20 | 280 |

| 2019-20 | 2020-21 | 289 |

| 2020-21 | 2021-22 | 301 |

| 2021-22 | 2022-23 | 317 |

How to Calculate the Indexed cost of purchase or indexed cost of Acquisition (ICoA)?

The indexed cost is calculated with the help of a table of cost inflation index as given above.

Divide the cost at which you purchased the Property/Investment by the index as on the date of the purchase. Multiply this by the index as on the date of sale.

ICoA = Original cost of acquisition * (CII of the year of sale/CII of year of purchase)

Let’s say you have invested in a debt fund in August 2014. Your investment amount was Rs 2,00,000 (20,000 units @ Rs 10 each). Seven years later, you redeemed your investments in June 2021, at a value of Rs 3,00,000 ( 20,000 units @ Rs 15 each).

Hence, when you sold your investments, the value of your investments was Rs 3,00,000. Your investment made capital gains worth Rs 1,00,000. However, you need not pay tax on this entire amount of Rs 1,00,000.

All you need to do is apply the formula.

- Cost of acquisition is Rs 2 lakh.

- CII number for purchase year (2014-15) was 240.

- CII during sale year (FY 2021-22) is 317.

This would mean that your indexed cost price of acquisition would be –> (2,00,000 * 317/240) = Rs 2,64,167.

As again, your Long term capital gains would come down to Rs. 35,833 (Rs 3,00,000- Rs.2,64,167), you will be taxed 20% of this amount (as compared to Rs 1,00,000 without indexation) which will again, greatly reduce your tax obligations.

Thus, with Indexation, you can enjoy the benefits of your own investments without losing an excessive amount of taxes.

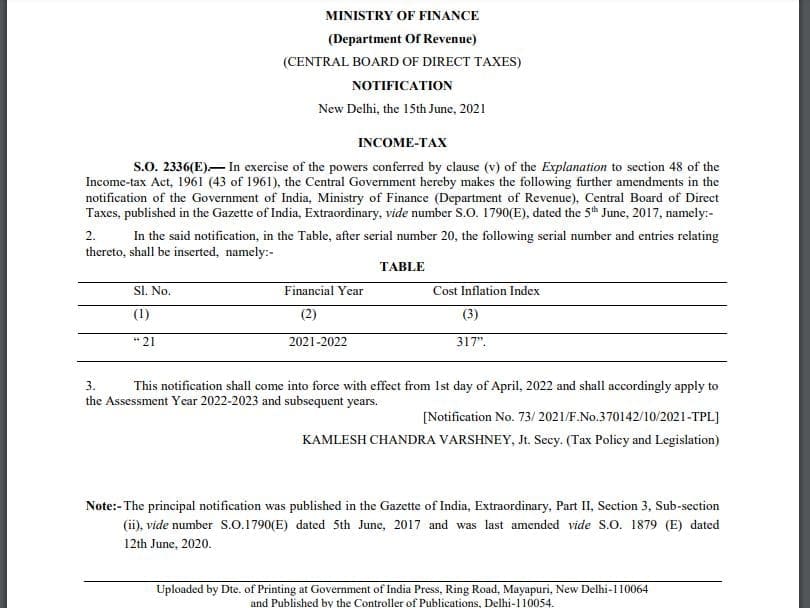

CII Index Value for FY 2021-22 / AY 2022-23 | Notification

Below is the notification issued by the Ministry of Finance on Cost Inflation Index for FY 2021-22.

Continue reading:

- What is Negative Real Interest Rate? | How Can Interest Rates Be Negative?

- What is Indexation of Mutual Funds and why is it important for you?

- List of all Popular Investment Options in India – Features & Snapshot

- How to save Capital Gains Tax on Sale of Land / House Property?

(Post first published on 27-June-2021)

Join our channels

Thanks for sharing Article one

Keep visiting relakhs, thank you!

Test comment

Thanks for sharing Article.

Hello Sreekanth ji, I read your article on Relakhs.com and I had a epf related query: I left my job after 2 yrs of service n have joined a new organization. Now due to some troubles in my current organization I am unable to transfer my old company epf account to my current epf account. Now I want to know what part of my old account where there was no contribution after 2 years is taxable that I have to declare in itr?

Dear Sreekanthji

I purchased a residential plot in 2007 and then constructed residence on it in 2010.

Could you please guide which year will be taken as a base year for acquisition of residential property 2007 or 2010 for calculating CII if house property is sold in 2121. Can I simply add cost of construction and make CII calculation from 2007 itself.

Thanks and regards. Ghansham Dass

A very informative article and I am really delighted to come across such an useful blog.

Hello Srikanth,

Hope you are doing well and doing good. I always follow your suggestion in MF and I never aware that you are writing very nice blog over real estate as well. since now I have decided to buy property in Hyderabad so have two question as below and if you can give your answer then it will help me.

1) What is the benefit if we give the half of the amount to builder in cash…

lets say.. flat price is 60 L and I will pay 30 L in cash (black) so in that case ultimately my registration price will reduce , so do you think that in this way we common man paying regular income tax have any benefit by converting our white in black.

2) What’s your thought on the home loan repayment? is it wise idea to repay loan in between or that same amount can be invested in Mutual fund or any other scheme where we can get higher return

Let me know your thought on the above question.

Regards

Mihir

Dear Mihir,

Thank you for being my blog’s loyal reader!

1 – There is no benefit by converting white into black money. Try your best not to do so! I know its tough to find such deals, but you can try for a deal where white component is HIGH!

2 – There is no right or wrong or straight forward answer to this. It is dependent on many factors!

For ex: If one has already paid EMIs for more than half of the loan tenure then advisable to continue with the loan EMIs.

You may go through this article @ Investing in Mutual Funds while paying Home Loan EMIs | Cost-Benefit Analysis